($FRMO) FRMO Corp: The Most Important Things - Part 3.1: Bitcoin is the "better money"

What needs to go right, else nothing else matters?

“I think the key ingredient of that is focusing on what is the risk you’re taking. I think a lot of people get in a lot of trouble because they do a transaction and they don’t understand what the risk they’re assuming is when they do the transaction. What he taught me more than anything else was, look at the deal and figure out where is the vulnerability? Where is the assumption you’ve made that has to be right in order for the deal to work? [...] The only real issue was, could you or could you not rent the office space? If you could, the deal was going to work. If you couldn’t, all the other stuff didn’t matter.” — Sam Zell on learning from Jay Pritzker

What are the top things that render all other issues irrelevant for whatever current problem you’re looking at? IMO, the most important things for the success of FRMO, the things that most need to be true for the investment to work out in the long term1 are (in order of what topics I think are the least to most opaque) are...

That the commod shortages that are being bet on at FRMO — mainly oil — are "structural" (mentioned in HK's 4Q2021 and 1Q2022 commentary reports), which in the context of HK/FRMO articles or transcripts kinda hints that demand destruction is not a long term concern, but rather that the supply vs the world's non-discretionary demand is so far apart as to not be affected by the any monetary policy in the long run. FRMO’s main oil holding is $TPL.

The Fed is trapped and can't / won't / might not actually want to raise rates in a too-serious way to kill inflation — and even if they do raise rates it would create a economic and political situation wherein those rate hikes would not last long or… see #1.

FRMO’s main BTC moon-shoot thesis works out (or is at least directionally correct) — management recently mentioned in the 3Q2022 CC that crypto (not TPL or oil) was their most important investment view. While they hold a lot of various little call options that could end up paying out significantly in the longer run, FRMO’s main BTC holding is though $GBTC. ********** UPDATE 20230618: BlackRock has recently applied for a Bitcoin spot ETF to trade in the US; their record for having ETFs approved by the SEC is 575 to 1; this twitter thread had an interesting POV linking BlackRock’s timing to their supposed expectation of a crackdown on large and less-reputable crypto exchanges Binance and Tether, which would allay SEC concerns of manipulation in the crypto marketplace. This is all interesting as Grayscale is currently in a lawsuit with the SEC that is still ongoing over converting their own Bitcoin trust into a spot ETF and it seems unlikely and inconsistent if BlackRock gets their spot ETF, but Grayscale does not. Furthermore, having competing sport ETFs on the market would likely force Grayscale to lower their existing management fees. **********

BTC is not going to be outlawed2 and that Tether does actually have all the USD required to back each USDT (which is important since USDT makes up 60% of BTC's inflow volumes at the time of me writing this (20220501)) — ie. that Tether is not some scam3 to pump the market cap of BTC using USDTs that are not actually backed by any USDs or other asset4. ********** UPDATE 20230125: Note that Stahl does not care about Tether one way or another re. BTC’s longterm value (expressed in past FRMO CCs) and this sentiment is echoed similarly by his thoughts on the FTX situation (see https://seekingalpha.com/article/4570490-frmo-corporation-frmo-q2-2023-earnings-call-transcript). **********

Here I cover what Stahl and Bregman et al at FRMO/HK have said on these topics as well as some notes from other POVs on the subject.

Table of contents

First, some shorthand acronyms

Just want to have the option of using these vs typing out the whole phrase in case I end up frequently referencing them in this post.

BTC = Bitcoin (Note there is technically a difference between Bitcoin the protocol and BTC, the abbreviation for the Bitcoin cryptocurrency itself, and I use the terms interchangeably, but it should be relatively easy to guess which is being referred to by surrounding context in this post.)

TX = transaction

SoV = store of value

MoE = medium of exchange

PoW = proof of work

PoS = proof of stake

Stahl’s Stance on Bitcoin

“You’re looking at an exchange rate, so the question is, how many bitcoin can a dollar buy? You’re seeing that the dollar keeps buying less, and less, and less bitcoin. Meaning, if you want a bitcoin holder to part with a bitcoin, that person wants more of your dollars to encourage them to part with that bitcoin. The majority of people think that the bitcoin people are irrational, and in general the bitcoin people people think the fiat buyers are irrational because their money is being debased. They’re willing to invest their money in a bond that clearly provides a negative rate of return. There are bonds that actually have negative interest rates in the world. Quite a few of them. Who’s crazier? That’s the question.” —- https://www.frmocorp.com/_content/letters/2021_Q2_FRMO_Transcript.pdf, Murray Stahl

FRMO chairman Murray Stahl was one of the earliest institutional investors in Bitcoin, first building his position in 2015-2016 around the same time as Bill Miller5 —and at age 68, Stahl may be one of the oldest institutional guys to have a bullish outlook on Bitcoin (just behind Miller by a few years). After reading through the FRMO conference calls and Horizon Kinetics quarterly commentaries, Stahl’s investment thesis on Bitcoin6 basically appears to be a combination of the ideas (and I’ve added stars next to what I think are the most important points) that...

★ ********** UPDATE 20230726: Around the time the Bitcoin whitepaper landed on Stahl’s desk, FRMO was looking for big investment opportunities. Many possible industries they were looking at were either already quite mature, saturated, or penetrated —recall Peter Thiel’s advice that “competition is for losers” and consider that any new semiconductor, soft drink, or restaurant would have to ultimately grow by taking market share from existing large incumbents— or not within their circle of competence (relative to other players already in those space). Crypto offered an opportunity in an emerging industry that could be entered without risking too much capital up front (ie. could be experimented with incrementally rather than requiring large radical investments), where all entrants where basically still at the starting line and that Stahl was confident that FRMO could learn sufficiently.

+ ★ ********** UPDATE 20230726: Stahl mentions in the Q3FY2023 earnings call that there are very few businesses that offer the opportunity to convert capital assets into permanent ones. Royalty businesses partially have this feature in that capital used to acquire land or mineral (or other ownership) rights produce permanent rights, in this case, in the form of minerals, oil, etc that expands/multiplies as new technologies for discovery, economical extraction, and use cases are discovered by the downstream participants at no cost to the royalty owner. However, these minerals ultimately need to be exchanged for cash. Bitcoin mining is an even more pure capital-assets-to-permanent-assets business in that mining rigs (purchased with BTC) ultimately “convert” into (more) BTC which, for various reasons addressed later, Stahl views as a valid and valuable store-of-value or currency in itself.7

(The common argument that Bitcoin mining and BTC is not a productive asset (as often stated by the acclaimed Buffet and Munger), in my opinion, is somewhat akin to being an investor in 1965 and saying that the tiny island nation, a “malarial swamp with no assets”8, backing the newly-independent Singaporean dollar was worthless and did not represent any material productive assets. Stahl seems to believe that, in time, a BTC will be as good as gold or any other fiat currency.)

**********

+ ★ The Fed has no choice but to inflate away US debt and can't raise rates (certainly not above inflation rate) due to the interest and entitlement expenses that would befall the US9, see…

The Fed is essentially orchestrating a kind of informal debt write-off for both the government and other individual and corporate debtors.

“In September 1797, two-thirds of the [French] national debt was written off and one-third was consolidated in the registry of the national debt. In effect, the government was willing to pay thirty-three cents on the dollar to its creditors. That act further undermined the faith of the common people in their government and they hoarded their gold currency with even greater urgency.” —- “The Gold Book”, Pierre Lassonde

+ ********** UPDATE 20230726: Bitcoin is a fixed issuance (crypto) currency and thus not at risk of the debasement that every central bank in the world is enacting on their local currencies. Even gold is not a fixed issuance form of exchange in the sense that new gold as always be discovered (eg. via deep-sea mining, laboratory synthesis, or even via asteroid mining some day), consider the inflation of the 16th century Spanish Price Revolution caused by the influx of gold imported from the Americas; Bitcoin will only ever have issued 21MM BTC. **********

+ BTC is the largest-network cryptocurrency of all the other comps, which by Metcalfe’s Law should help defend BTC’s existing dominate position among fixed-issuance, PoW cryptocurrencies (see references here and here, just use word-search to find the exact references).

+ This scale also helps protect Bitcoin’s PoW TX validation system from 51% attacks better than any other competing PoW cryptocurrency.10

+ The Bitcoin protocol is the least energy intensive11 crypto (PoW) block validation protocol. (Of course, I don’t think that Bitcoin miners should even need to justify how they legally use the energy they freely (and without government subsidy) pay for in the first place, which seems to be a common requirement from grasping Bitcoin critics almost exclusively only when that energy is being used to mine BTC).

+ ★ BTC blockchain and POW protocol solves the authentication (Byzantine General’s) problem of trust12 13 otherwise impeding effective competition of privately issued monies, per Friedrich Hayek’s “Denationalization of Money”14 — which essentially argues for a libertarian view of currency creation in which private entities can create their own monetary system and money that freely compete for people's adoption (of which inflation-protection is presumed to be a desirable quality by people free to choose); Hayek —whose home country of Austria suffered greatly from inflation after WW1— largely blamed inflation and the centralized intervention responses by governments thereto for causing instability and unemployment cycles in capitalist economies.

How, then, to achieve monetary stability? Milton Friedman, and recently many others, have urged a monetary rule, embedded where possible in a "monetary constitution," so that the growth of money is steady and predictable. There can be no doubt that such a rule would end the grosser failures of monetary management. But why do we need to regulate our suppliers of money? Here competition comes in. For regulation of an industry — by government, regulatory agency, or rule — can be defended only if the industry is not regulated by competition. In general, competition will deliver the best attainable outcome. Why not in money? —- “Denationalization of Money: The Argument Refined”

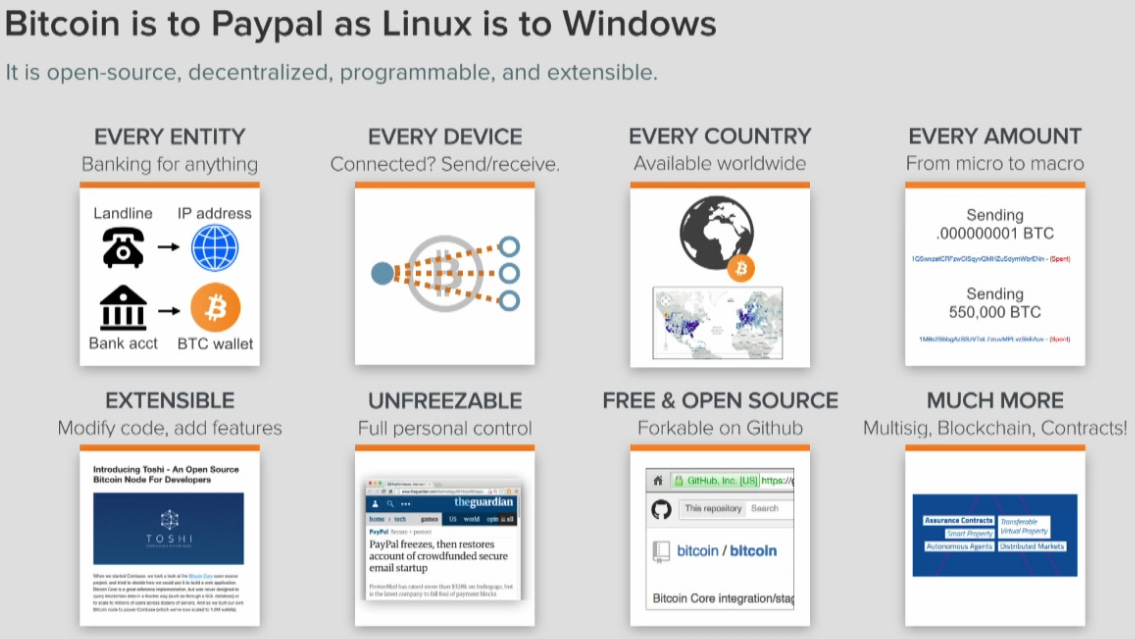

+ Bitcoin is “consensus money”. BTC has no centralized, reachable founders, foundation15, issuers, or officers and no centralized governance for how it's developed; You could say that Bitcoin's development has been via an “emergent strategy” (after it’s initial immaculate conception by whoever Satoshi Nakamoto is/was); and even if, for example, Bitcoin Core devs started pushing hostile changes to the code base affecting Bitcoin's blockchain (or even changes that just seemed like bad ideas)...

+ ★ …BTC is open source and thus its code base is openly and globally auditable; and updates to the Bitcoin protocol must be adopted by consensus of existing full-nodes in the network. When the Bitcoin Core code is changed, existing full-nodes in the network need to actually accept/adopt that update. If the code change affects the main rules of how the Bitcoin blockchain works (eg. changing the total, fixed, BTC supply limit) you end up with a hard fork16 and you, as a BTC holder, would just now have your original BTC plus some pro rata amount of whatever new hard-forked BTC-offshoot cryptocurrency was just created by the blockchain code change; and if in the end that code change turns out to actually be superior, you are no worse for wear since you got those units (and for free) — so there's some free optionality in owning BTC outright vs GBTC.17

+ ★ Bitcoin’s creator —in a quasi-Jesus-like manner— gave the majority of its value (ie. the ability for anyone who was aware of Bitcoin to mint actual BTC from the outset and the development work that had to be done up front to create the Bitcoin protocol) at inception, to the miners/validators of transactions that supported the network (rather then simply allocating value to themselves at the outset)18 —something that any competitor is economically disincentivized from doing and thus hindering new entrants’ ability to pose a threat to BTC’s adoption19. Bitcoin launched with no pre-sale and pre-mine or any other kind of free BTC distribution to “founders” beyond the equal opportunity for those who knew about it to elect to mine the —at the time novel and unproven— cryptocurrency, this included Satoshi himself; it was announced for anyone to interact with on the P2P Foundation online forums20 and Satoshi himself waited until other has mined blocks first before mining for himself.

********** UPDATE 20230803: “Everything other than bitcoin,” Gensler told me, “you can find a website, you can find a group of entrepreneurs, they might set up their legal entities in a tax haven offshore, they might have a foundation, they might lawyer it up to try to arbitrage and make it hard jurisdictionally or so forth.” In other words, there are people behind these cryptocurrencies using a variety of complex and legally opaque mechanisms, but at the most basic level, they are trying to promote their tokens and entice investors. (Bitcoin, because of its unique history and creation story, is fundamentally different from other crypto projects in this respect.) —- https://nymag.com/intelligencer/2023/02/gary-gensler-on-meeting-with-sbf-and-his-crypto-crackdown.html **********

Barring this, to pull people away from BTC, a new entrant would need to have some really good feature(s) they’ve implemented, but then…

+ …again, BTC is open source and thus —aside from having a code base that’s openly and globally auditable— can implement and incorporate any new features if full-node consensus decides to adopt it. Of course, a new entrant could be a private entity and thus keep the implementation of their features a secret, but then any private crypto BTC-competitor would fail the trustless criteria and thus fail the Hayek authentication problem and thus be inferior to BTC.

+ Gresham’s Law (ie. bad money pushes out good money ⇒ people will hoard BTC; the assertion here being that BTC is the better money that people will store as long-term savings). This hoarding behavior can be seen playing out in real time when looking at the actual blockchain21 — an interesting piece of empirical data made visible by the public aspect of the blockchain.

+ ★ Law of no arbitrage bringing BTC’s total market cap to be >= that of all the world’s gold (in the more conservative success mode) or all fiat (in the most optimistic success mode) (see references here and here22) . It's possible that, in such a success mode, BTC could also significantly eat into other SOV asset classes, like investment real estate, art, etc.

⇒ Bitcoin is / will remain the best (read as: “market leader”) SOV crypto and be recognized as the “better money” vs all fiat23

⇒ If/when inflation via currency debasement takes hold for the long term across the world, BTC will be the best deflationary alternative global asset (per the idea that BTC solves for / allows the trustless “denationalization of money”) and people will use/exchange fiat and horde/accumulate BTC (per Gresham’s Law)

⇒ The value (or purchasing power) of BTC goes way up. In Stahl's mind, the market cap of BTC could reach the value of the GDP of whole economies or segments of economies (ie. Bitcoin’s TAM) that adopt BTC over fiat (by the Law of No Arbitrage) which he sees as eventually everybody / the whole world, into the value of millions of dollars per BTC. I have a slightly less optimistic view on BTC’s endpoint that I’ll go over a bit later in this post or a subsequent one.

…and as the purchasing power of BTC increases, you can exchange BTC itself for more good/services (vs all other fiat)

…and iff/as BTC becomes more widely accepted/adopted24, then subsequent/concurrent legal and technical infrastructure should continue to be built out and make TXing w/ BTC easier in the long run (though taking this to the extreme is really more of a MOE Bitcoiner’s POV as opposed to Stahl’s SOV investment thesis). This would remove the need to exchange BTC back to USD in order to actually extract wealth from your BTC. In such a scenario, it could also become possible to earn relatively low-risk BTC yields on your BTC.

“All substance is energy in motion. It lives and flows. Money is symbolically a golden, flowing stream of concretized vital energy.” —- The Magical Work Of The Soul

.

********** UPDATE 20230727:

I raised some of the questions I posit here during the Q3FY2023 FRMO earnings call (re. Hayek, Gresham’s Law and Theirs’ Law) and Stahl’s response was that —irrespective of Hayek et al— his Bitcoin thesis boils down to the idea that the post-WW2 fiat system is breaking down and that something will need to replace it; he sees cryptocurrency and Bitcoin as the best alternative available —better than gold (given BTC’s better money-like features and codified scarcity) and better than any kind of Keynesian bancor bundled commodity standard. This comes with the underlying assumption that the best ideas ultimately (at least the highest probability to) win out and do so within a survivable amount of time.

“I had absolutely no comprehension of the power of markets versus politics. The policy makers didn’t understand that either. I think, as is often the case, policy makers don’t understand that they are not in control. It’s not that speculators are in control, either, but rather that fundamentals actually matter.” —- Colm O’Shea, “Hedge Fund Market Wizards”

He views blockchain-enabled, proof-of-work-secured digital scarcity as better than any other alternative system put forth thus far and ultimately believes that —in the fullness of time— the government will seek to hoard BTCs and will thus allow people to transact and pay taxes (likely without any capital gains tax applied) using BTC in order to acquire the cryptocurrency for themselves.

“““

We just think that a system of digital scarcity is superior to any other system. That’s the only assertion we’re really making. But if you want me to guess what’s going to happen, it’s that governments, for purposes of expenditures, are going to use their fiat currency. For purposes of revenue, they —let's say it's the U.S. government— will accept the dollar, of course, as legal tender for payment of taxes. But I believe one day they're going to accept bitcoin, and ultimately, I believe the government is going to hoard it.

I believe the day is going to come when people will be able to pay their taxes in bitcoin. If that happens, and if you own below-basis bitcoin, the government might even let you pay taxes without realizing the capital gains on its appreciation, to encourage you to pay with it so that the government can collect a store of it. It will build a holding of crypto and use it as a device to try to rescue governments from insolvency.

I really believe that's going to happen, because the way it's going, you have a lot of governments that are on the road to insolvency. They won't really default, they'll just keep creating currency. But the financial situation of most governments in the world is actually pretty dire. That's how I think it's going to ultimately evolve. So, we're not making a bet on hoarding or the opposite. All we're willing to say is that digital scarcity is better than the available alternatives, and that's about as far as it goes right now.

””” —- Murray Stahl, FRMO Q3FY2023 earnings call

A rather bold bet, I think. As SEC Chairman Gary Gensler puts it…

“History tells us throughout — through antiquity to now — that economies coalesce around one monetary unit,” he said. “There is a network effect to having one unit that we humans accept as a medium of exchange and unit of account — a store of value — one unit. The two things governments do since Genghis Khan,” he observed, “is basically say, ‘This is what’s accepted for your taxes, and it’s accepted for all debts, public and private.’”

“I don’t think there’s much economic use for a micro-currency, and we haven’t seen one in centuries,” Gensler said. “Most of these tokens will fail, because the question is about these economics. What’s the ‘there’ there?” —- https://nymag.com/intelligencer/2023/02/gary-gensler-on-meeting-with-sbf-and-his-crypto-crackdown.html

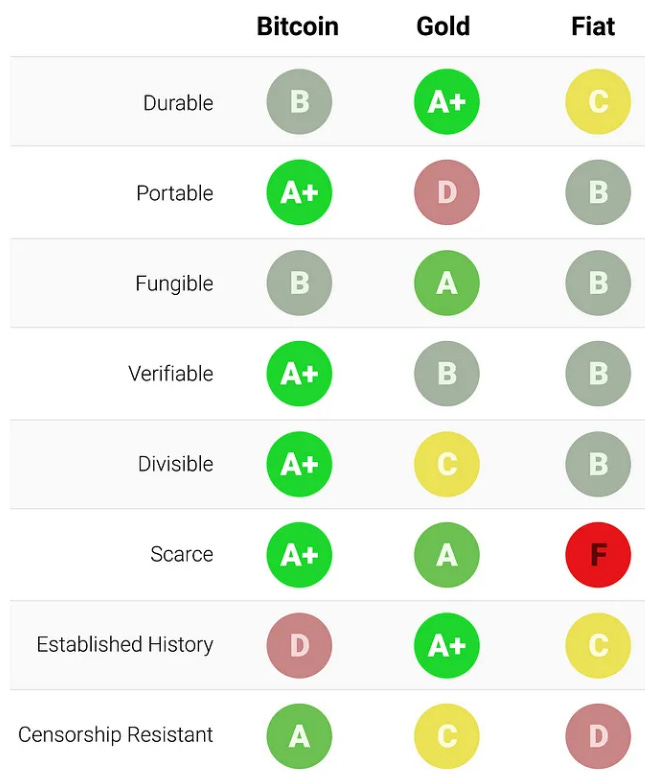

(PS. On the issue of gold, I’d also like to note that while many like to point out that gold also has industrial uses that separate it from Bitcoin, those industrial uses only account for less than 10% of gold’s value):

Estimated global gold consumption was jewelry, 47%; physical bar, 21%; central banks and other institutions, 14%; official coins and medals and imitation coins, 10%; electrical and electronics, 7%; and other, 1%. —- “Mineral Commodity Summaries 2022”, U.S. Geological Survey

**********

.

For the more out-there aspects of where Stahl thinks Bitcoin and blockchain technology is going —you know, aside from overthrowing fiat money— you can listen to a 2021 interview Stahl gave here25. IMO, of the many use cases26, one of the most interesting propositions and —again, just my opinion— the one with the highest “expected value” (in the sense of being highly society-changing as well as being highly probable) discussed in this interview is the particular dis-intermediating effect blockchain and public ledger transactions will/would have on the traditional many-to-one, individual-to-Google-to-advertisers relationship; Inverting it into a one-to-many, individual-to-advertisers relationship wherein advertisers directly pay individuals for the right to advertise to them based on their blockchain transaction history rather than Google acting as a gatekeeper (timestamp 01:09:41)27. My second highest “expected value” bet would be some form of snapshots of the world being encoded into the blockchain.

There’s some obvious gaps in this vision like “how exactly are advertisers going to find / search for the exact people they want to advertise to?” and “What about people who prefer to keep certain TXs private?”, but I think a lot of that will be taken care in the course of time by the open-source community or commoditized via entrepreneurial exchange creators (ie. the continued securitization of everything)28, so long as the raw public blockchain data remains and as culture around the blockchain (if Bitcoin manages to survive long enough —which it's done a pretty good job of doing thus far29).

********** UPDATE 20221114: TBH, I think that the most impactful innovations that will emerge out of Bitcoin and blockchain tech have not been invented or conceived of yet or implemented at any commercial scale. **********

Supplementary commentary

John Pfeffer —FYI, a former KKR partner, for anyone who’s ever read “Barbarians At The Gate”— has a similar POV on the value of BTC. He had an interesting interview w/ Invest Like the Best podcast where he talks about a unique difference of BTC (as a SOV) vs other cryptocurrencies like ETH et al (which are competing more in the MOE space):

“I'm actually hugely bullish about Ethereum. I'm hugely bullish about all of these things. I think they're going to scale. I'm a huge bull from a technology perspective. The question is as an investor, am I a bull in owning those assets? And I think they're not great businesses to own as assets. There is however, this great business, which is store value money. It's not only a great business that it's going to capture a lot of value, but also it's actually quite simple. The tech risk isn't that high. So it's a good business in many respects. And Bitcoin is laser focused on that and does it extraordinarily well. There's a tremendous consensus around that fact. And no one's really competing with that.” —- Pfeffer on the hoarding value (or lack thereof) of ETH vs BTC

I think this little snippet helps clarify one of the implicit, differing narratives in BTC: That between the SOV Greshamists (who see BTC more akin to a superior form of gold (so long as modern civilization remains intact30)) and the MOE, hyper-bitcoinization Theirsists who want to TX everything in BTC and build things like the lightning network (as well as spawning Litecoin, Bitcoin Cash, et al) for greater TX throughput support and thus (as Pfeffer would put it above) are actually competing with ETH for MOE leadership —something that Stahl has expressed little interest in31. Stahl talks a bit about this here32:

“My personal perspective on the issue of bitcoin speed and capacity is that the idea was to create a substitute for fiat money that you would hold for a long period of time. The idea was not to make it, initially, as liquid as, say, fiat money. The idea was to avoid the danger that big corporations would come and dominate the system — like what happened to the internet.” —- https://frmocorp.com/_content/letters/2021_FRMO_Transcript.pdf

“In accordance with Gresham’s law, what people are expected to do — and which they do — is to hang onto their gold, and transact in or let go of their dollars. They’re not really supposed to use the gold for transactions, except occasionally. […] It’s not going to be MasterCard, it’s not going to be Visa. That’s not what it was intended to do. I think scaling misses the whole point. […] [Y]ou see what happened — no one, or at least not very many people, are vitally interested in the forks. Now they think that potential users are not vitally interested in a given fork because they didn’t scale it sufficiently; that if they’d only scaled it even more, then people would come to it. […] So, why in the world are they building these scalable networks for bitcoin? I have no idea what they’re trying to accomplish. I look at those efforts, because it’s intellectually interesting, but I don’t think it has a lot of impact on bitcoin.” —- https://www.frmocorp.com/_content/letters/2022_Q3_FRMO_Transcript.pdf

TBH, while I think BTC is very interesting, from an investment POV it’s presently a bit of a hanging chad on an otherwise interesting, inflation-hedged, jockey-stock investment narrative for FRMO because —while FRMO’s cost basis / initial weighting on the majority of their crypto-based holdings relative to their other assets is tiny compared to the prices they are marked to market at now— this risky, marked-up asset class constitutes a significant portion of their book value. They essentially made a small VC bet on a startup monetary asset while it was still in its very early development in 2015-2016 that ended up seeing explosive growth / fund flows. Congratulations to them, but any new incremental investment in FRMO shares means you’re coming into an FRMO with ~7.5% of TBV made up of GBTC33 (w/ a few smaller crypto bets on the B/S as well) vs the few basis points of crypto allocation FRMO started with.

However, this is much less exposure than previously, given the crypto-crash that’s recently gone down in the markets since I initially drafted the notes for this post. In large part due to this crash (but not entirely, as there are other issues the entire market is working through ATM), $FRMO has fallen ~20%. This actually makes this a more attractive investment IMO as you get more of a pure-play exposure to Stahl & co’s more traditional inflation-hedging, hard-asset, asset-light business ideas, while still maintaining the upside optionality of the crypto stuff ultimately working out in time.

And who knows? This could just be the end of the beginning for BTC or —as FRMO management has repeatedly acknowledged themselves— the whole Bitcoin experiment could also fail. Of all the businesses adding exposure to cryptocurrency, I’d say FRMO presents a good balance of management I trust + large enough exposure to make a difference if things go right. For this reason, I would either pretend that the GBTC portion of FRMO’s TBV could quickly drop to 0 and calculate that into your VAR or simply assume it from the get-go and just subtract that percentage from FRMO’s TBV when looking at it from a P/TBV POV when weighing whether to buy shares at all.

.

There’s also now the possible tailwind of global diversification away from the USD:

“What is money?” is a question that economists have pondered for centuries, but the blocking of Russia’s central-bank reserves has revived its relevance for the world’s biggest nations—particularly China. In a world in which accumulating foreign assets is seen as risky, military and economic blocs are set to drift farther apart. […] Weaponizing the monetary system against a Group-of-20 country will have lasting repercussions. […] Many economists have long equated this money to savings in a piggy bank, which in turn correspond to investments made abroad in the real economy. […] Recent events highlight the error in this thinking: Barring gold, these assets are someone else’s liability—someone who can just decide they are worth nothing.

The main point here —as it relates to Bitcoin— is that recent US sanctions on Russian reserves held in US-controlled banks is going incentivize countries to diversify their reserves away from the dollar and into a more neutral SOV. Gromen talks about the emergence of a Keynsian bancor, physical commodity-based system of settlements34 and this is similarly echoed in recent writings by a Zoltan Pozsar (the phrase “Bretton Woods 3.0“ has been floating around a lot recently). However many cite some interesting difficulties in supporting such a global settlements system regarding actual transactions of physical commodities (though, note that Bitcoin would not have this issue)35 —and I recall that Stahl himself has directly disagreed with Pozsar's Bretton Woods 3 thesis36:

********** UPDATE 20230205: What is talked about in these critique of Pozsar is not quite the interpretation I understand him as having re. the term “Bretton Woods 3” as he clarifies here (in case the video loads wrong, the relevant timestamp is at 1:00:02): **********

Questions / concerns

I’d like to get an update on management's thoughts on the apparent non-correlation of recent Bitcoin prices vs inflation and CPI numbers — given the rather large drawdown that BTC has seen while CPI numbers remain elevated. Taken in hindsight, it appears to be / have been behaving like any other high-beta, high-duration, liquidity-lottery winner of the Fed's QE financial asset inflation policies.37 ********** UPDATE20230118: Stahl has mentioned that he wrote a paper warning about the excesses of about the impending dot-com bubble in the early 2000s titled "The Infinite Bear Market", I have a copy but have not gone through it. In any case, it appears he’s at least cognizant of this idea and it should be noted he was not caught up in the previous Bitcoin mania. **********

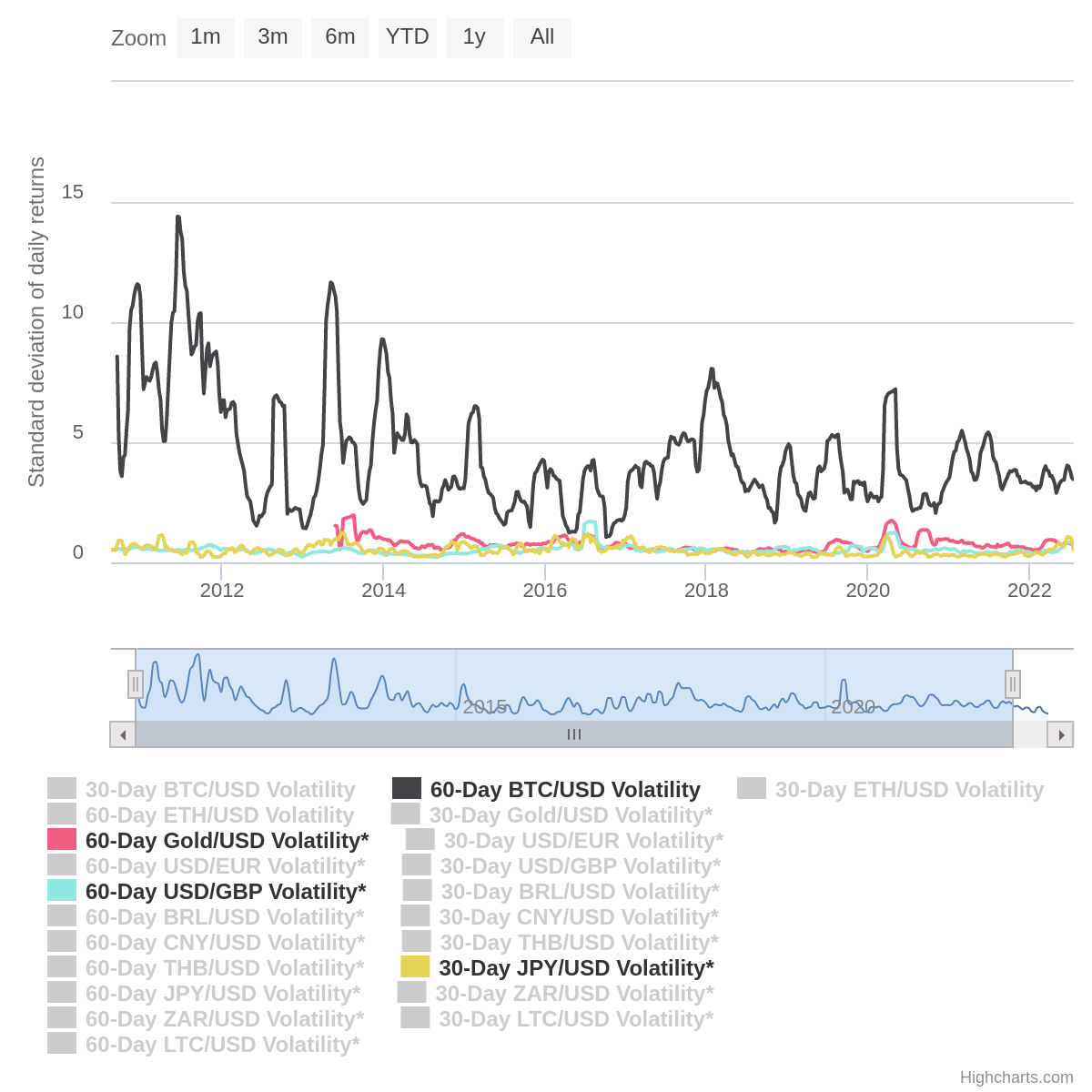

One of Hayek’s requirements for a denationalized money was stability of purchasing power, which BTC certainly has never had.

(Though you can also observe in the chart above that BTC/USD price volatility has also been dropping over time).

On the topic of Hayek and stability, IMO it’s not totally clear that a managed 2% inflation rate (eg. that offered by the Fed’s ostensive mandate) is any less stable or predictable —at least in theory, as looking at something like the BigMac Index vs CPI we can see some evidence for the idea that this 2% inflation target is not even really being achieved in practice— than a programmatically enforced 0% inflation rate applied to just the money itself (as with Bitcoin).

In the previous FRMO conference call, management commented on BTC's relation to Gresham's Law, subsequent hoarding behavior, and the lack of any need for a more scalable BTC network. By a similar economic law — Thiers' Law — when there is no enforcement of like treatment between differing currencies (which was not the case in 16th century England's Great Debasement that management has cited in the past wherein coins were gradually stripped of their precious metals content while still decreed to be worth the same nominal value as any other coins), then good money drives out or is used versus the bad (the opposite of Gresham's Law). Now, I may be confusing the situation or the chicken vs the egg here, but this seems to be the situation presently where 1 USD denominated in BTC is not legally treated the same as 1 USD in fiat. Under Thiers' Law, working towards network scalability makes sense in that it would go towards facilitating BTC's medium-of-exchange use cases in a similar manner to the dollarization that can be observed in cases of hyperinflating EM economies. I’d like to see management comment on why they believe the present conditions are such that Greshm's Law applies in the case of BTC, as opposed to Thiers' Law (wherein BTC hoarding would actually be seen as a failure) — ie. does hoarding BTC and acting in accordance of Gresham’s Law even make sense for the current situation (again, I may be confusing the situation or the chicken vs the egg here)?38 See https://bitcoinmagazine.com/culture/demanding-payment-in-bitcoin.

********** UPDATE 20230118: Additional stuff to add to the above concern: From the Q3FY2022 FRMO conference call + an interview Stahl gave a few years back, it appears that management is betting on the store-of-value case as similarly articulated by former KKR partner John Pfeffer for Bitcoin vs the medium-of-exchange case. In the former case, does Hayek's money denationalization even matter here --or even possibly hurt FRMO's BTC investment thesis-- since it appears to call for the dynamic of Thier's Law? In "Denationalisation of Money", see chapter 6 titled "The Confusion Aabout Gresham's Law", Hayek mentions that "Gresham's law will apply only to different kinds of money between which a fixed rate of exchange is enforced by Law" and that Gresham's Law "is not false, but it applies only if a fixed rate of exchange between the different forms of money is enforced", which does not seem to be the case in our world where a free market of global currency exchange exists39. Related to the store-of-value case, could we get management's thoughts on the value of gold (especially in the context of a world dominated by a single superpower)? In what seems to be further implicit support for a Thier's Law dynamic re. BTC's inflation hedge narrative, Hayek claims that "whenever inflation got really rapid, all sorts of objects of a more stable value, from potatoes to cigarettes and bottles of brandy to eggs and foreign currencies like dollar bills, have come to be increasingly used as money." (Notice not hoarded (as Gresham would predict), but used as money --which I assume means used to transact, eg. as a medium of exchange). In fact, as a practical example, in the previous shareholder call, Stahl mentioned that cryto mining companies themselves are transacting in BTC rather than USD (vs hoarding BTC). Given this information, I wonder how much of BTC hoarding is based on lost keys or on Gresham’s Law bandwagoning delusion? **********

Management has been rather bearish on Ethereum in the past, citing the difficulty in scaling given ETH's energy costs and — more recently — proof-of-stake policies. Could management give their thoughts on ETH's outsized developer community vs other cryptocurrencies — including BTC — as well as its dominant network size measured in Total Locked Value (TLV)? You can read more about this here: https://traviswiedower.com/2022/06/06/my-ethereum-investment-thesis-fundamentals-and-flows/

SEC chair Gary Gensler — who can certainly be said to know something about BTC considering that he used to teach a class on the subject at MIT — has consistently rejected BTC spot ETF proposals. I’d like to see management comment on some of the concerns he points out in his SEC order (File Number: SR-CboeBZX-2021-051)) on the reason for denying ARK Invest's BTC spot ETF as well as the recent $GBTC spot application rejection. You can read more about the ARK rejection (from a BTC skeptic) here and the GBTC rejection (from a BTC bull/VC) here (@ 00:34:59).

Is it a problem that over 50% of all Bitcoin nodes are hosted in unknown geographies (ie. over 50% of Bitcoin nodes are running on the TOR network)? Also, how does management think about the lack of clawbacks of BTC in the case of fraud and how that hinders adoption? What are management's thoughts on the concentration of mining pools in the Bitcoin network and the geographical concentration of those hosted pools? See https://bitnodes.io/nodes/?q=unknown-country.

Though it should be noted that mining pools don’t necessarily have custody of the mining rigs that are using the services of the pool and miners can leave those pools if those pools are no longer acting in their interest.

********** UPDATE 20231212: See Stahl’s answer at Questioner 7 here: “As far as the nodes are concerned, if we knew exactly where every node was, it would be a lot easier to hack. If we want a system that's so far, at least, impervious to hacking, why do we want it to be public knowledge where every node happens to be, so that someone maybe a bad state actor with the resources to devote to that problem—could actually figure out a way to hack it? I don't know what nation would undertake it, but there are nations with the resources that might try. The whole idea is that anonymity—or, let's say, independence or resistance to a certain amount of scrutiny—is a good thing if you want to protect the currency from those who would otherwise seek to control it.” **********

“Solon said well to Croesus (when in ostentation Croesus showed him his gold), ‘Sir, if any other come that hath better iron than you, he will be master of all this gold’” (The Story of Philosophy, Will Durant (on Francis Bacon)).

One POV on BTC I often think about is this40…

It was 1967 Buckminster Fuller predicted Bitcoin and new wealth. “I'll talk about something that would be one of the realizations by 2018 a realistic—scientific accounting system—of what is wealth. Wealth isn't the gold of pirates—wealth is energy" 1967.

It was 1967 Buckminster Fuller predicted Bitcoin and new wealth. “I'll talk about something that would be one of the realizations by 2018 a realistic—scientific accounting system—of what is wealth. Wealth isn't the gold of pirates—wealth is energy" 1967.I often hear the idea that —as a sort of equivalence to a common push-back to BTC’s, theoretically, nationless backing— the USD is not really backed by anything (this is not a super consensus argument, but common enough that you see it pretty frequently). However, the USD is backed by the combined energy of the human and material capital of the US DoD…

This is what’s really backing the USD —and it’s managed to make the US the world superpower

Proof-of-war vs proof-of-work.

As a very simplistic exercise, we can roughly compare the pure energy backing of each currency in this sense by comparing the Bitcoin mining network energy per BTC to the aggregate energy consumed by the DoD per USD (IDK how to factor in the energy cost of the associated human assets, banking industry / infrastructure, etc, but I'd guess in this case the DoD uses more than the Bitcoin network) to get some directional or magnitude sense41 of an energy-based USD/BTC exchange rate. Using rough 2021 numbers42, we get something like:

(105B kWh / 21MM BTC) = 5000 kWh/BTC vs…

( ((915T Btu (1 kWh/3412 Btu)) x 0.77) / 2041B USD ) = 0.101172 kWh/USD

Does this mean that BTC should really only be worth closer to (5000/0.101172 =) 49421 USD? Maybe you could think of this as BTC’s “book value”? By this logic, we could solve for how much BTC should be worth relative to a USD by solving for…

(Eb / Cb) / (Eu / Cu) = BTC/USD energy based exchange rate, where

Ex = energy “used to secure” currency x

Cx = number of circulating currency units

As of this writing ~19MM BTC has been unlocked in total43 and the numbers I see have “BTC HODL rates” at ~70-80% of total supply44, so with 5.7MM BTC freely circulating, that's still just a BTC/USD kWh-based exchange rate of $182,076.00 USD/BTC.

Conclusion

Something that people seems to lose track of is that Bitcoin is not an all-or-nothing bet. You don’t need to invest 100% of your portfolio in BTC or adjacent Bitcoin industries in order to get an allocation into your portfolio.

IMO, BTC is a VC type bet (on a startup, market leader in the "monetary asset" space), so size your risk and adjust your reasoning accordingly (this video and slides may be helpful in reasoning about the investment).

Suppose you think BTC has a 7.5% chance of becoming valued (roughly) equivalent to the total gold reserves market and some portion of sovereign FX reserves (which is generally my own personal success-mode destination for BTC) —you could even add some multiplier for BTC’s various superior verification and transfer features over gold (and maybe even add in some of the investment real estate market cap if you were optimistic about the SOV case). Just using John Pfeffer’s 2017 $260K-$800K/BTC price range, that would constitute a 13-40x increase from BTC's current price. Note that your actual rate of return may vary depending on how long BTC adoption takes, if it happens at all (eg. a 27x endpoint return in 20yrs would mean a 18% CAGR, and so on).

How much of a portfolio should one bet on this? We can use the Kelly Ratio formula (https://en.wikipedia.org/wiki/Kelly_criterion), which IMO actually works well here since in the fullness of time —like in Black Jack betting, for which Edward Thorp originally used Kelly Ratios45— betting on BTC is a ‘you either win the bet or lose 100% of your cost basis’-type of bet in the long run.

So, in this example, for this assumed 7.5% probability of success, you'd only want to bet 4% of your total bankroll, despite the massive (nominal) asymmetry of the bet.

You can do this for whatever —ultimately arbitrary— probability value you want to attach to Bitcoin’s gold-market-parity success mode. A 5% chance of success would have the Kelly Ratio prescribing a 1.5% allocation and so on. (Note that Paul Tudor Jones, another notable big money manager, has mentioned wanting to hold a 5% Bitcoin position as part of a basket of inflation hedges and has written a bit about his thoughts on Bitcoin in mid 2020, here. Though also keep in mind that Jones made his name as a short-term trader who famously played psychological games with other traders.)

I think I’ll end it here for brevity. In the next part of this series, I will go over my own general thoughts on the investment case for Bitcoin and some of the other POVs from Bitcoin bulls and bears alike — I’ll try to avoid referencing any pseudo-visionary tech-bros or their simmering boomer counterparts46 as much as possible, but when it comes to Bitcoin that’s a hard thing to guarantee.

.

********** UPDATE 20220930: In case I don’t end up doing the part 3.2 addendum to this post, I’ll just note that my general thinking on the investment thesis on Bitcoin is based on these articles:

https://www.paradigm.xyz/Bitcoin_For_The_Open_Minded_Skeptic.pdf

https://vijayboyapati.medium.com/the-bullish-case-for-bitcoin-6ecc8bdecc1

https://medium.com/john-pfeffer/an-institutional-investors-take-on-cryptoassets-690421158904

… which does also align with Stahl’s POV of BTC hedge against the debasement of USD (and, by proxy, the various SOV assets valued in USD) which is described a bit in response to “Questioner 8 (cont.)” here. **********

Further Reading

https://www.frmocorp.com/_content/letters/2022_Q3_FRMO_Transcript.pdf — See “Questioner 4“ and onward for a discussion by Stahl on his views re. Ethereum, POS, and the value of Bitcoin.

“Denationalization of Money: The argument refined”: https://nakamotoinstitute.org/static/docs/denationalisation.pdf

https://www.frmocorp.com/_content/letters/2016_FRMO_Transcript.pdf (search "Gresham’s Law" there is also a discussion on Gresham’s Law here)

https://river.com/learn/terms/t/thiers-law/

https://river.com/learn/terms/g/greshams-law/ — “This is one of the reasons Bitcoin [narrative] has grown faster as a store of value than as a method of payment.”

https://bitcoinmagazine.com/business/what-is-nakamoto-greshams-law

https://bitcoinmagazine.com/culture/demanding-payment-in-bitcoin (Gresham’s Law vs Theirs’)

https://en.wikipedia.org/wiki/Gresham%27s_law#Reverse_of_Gresham's_law_(Thiers'_law)

Those examples show that in the absence of effective legal tender laws, Gresham's Law works in reverse. If given the choice of what money to accept, people will transact with money they believe to be of highest long-term value. If not given the choice and required to accept all money, good and bad, they will tend to keep the money of greater perceived value in their possession and to pass the bad money to others.

https://www.frmocorp.com/_content/letters/2022_Q2_FRMO_Transcript.pdf (search “It would be Armageddon for the banking system…”)

https://inthearea.captivate.fm/episode/murray-stahl-ceo-chairman-of-horizon-kinetics (TBH, in this interview you would think he’s talking about Jesus (equality, freedom, end of info asymmetry, flat orgs, etc), so you’ve been forewarned that you may want to roll your eyes at some points, if you are so inclined. In this vein, I’d also note — to anyone thinking of betting bigly on Bitcoin — that even Jesus was killed by the establishment.)

Note this is not including the various small call-option type bets they have such as MIAX, Winland Hld., their crypto mining operations, and Diamon Std.

********** UPDATE 20230526: For some more recent developments, see the section on “Regulatory Environment for Cryptocurrency” here, https://horizonkinetics.com/app/uploads/Q1-2023-Commentary_FINAL.pdf **********

You know… that guy at the end of “The Big Short”.

I don’t really have an opinion on this one way or another; some interesting commentary on Miller re. this period can be found here: https://www.investmentnews.com/bill-miller-back-on-top-but-questions-remain-after-financial-crisis-downturn-63706

This POV can be evidenced by the fact that the crypto mining company that Stahl is planning to bring to the OTCQX exchange tier this year is called “Consensus Mining and Seigniorage Corporation” (https://www.consensusmining.com/), “seigniorage” referring to the profit made by a government when it issues currency.

Charlie Munger’s own words, https://www.yapss.com/post/collection-charlie-munger-263-lee-kuan-yew-and-singapore-s-success

Many inflationistas like Luke Gromen, et al appear to get their main beats from or converge into Zoltan Pozsar’s Bretton Woods 3.0 thesis re. the ultimate destination of the structural inflation he foresees, whereas Stahl has directly disputed this idea.

********** UPDATE 20230329: I thought these videos were nice short descriptions of how Bitcoin is protected from a 51% attack: **********

As for proof-of-stake, there are many criticisms against PoS validation protocols as an efficient way to decentralize block validation with much lower energy costs — and I currently agree with them. See https://bitcoinmagazine.com/business/the-value-of-bitcoin-proof-of-work.

Furthermore, I find it odd in general that Bitcoin mining is one of the only times where people —who would normally be fine with the real estate and energy involved in, say, operating a movie theater or Netflix servers— suddenly decide that something needs to justify it’s energy usage; that miners needs to justify their usage of energy that they are freely paying for (and without government subsidy). I find this is often a good indicator of someone who has let their emotions get too involved in the investment question of whether Bitcoin can reach a true success mode in time and have strayed into the realm of seething grasping.

It is odd how Bitcoin has become a rather emotional topic for some investors and observers.

I don’t know how scalable bitcoin becomes and, frankly, I’m not in bitcoin because of scalability. The notion that there are going to be billions and billions of bitcoin transactions per day—well, if that’s what you’re looking for, there are hundreds of cryptocurrencies that can do that. Bitcoin is designed to solve one problem in the world of private money – because that what it is, private money. The idea of private money goes back hundreds of years. There was a limiting factor though, as stated in the book The Denationalization of Money by Friedrich Hayek, which is the authentication problem. What’s the authentication problem? Let’s say I, personally, created a currency. It doesn’t have to be crypto, it can be anything. I created a currency and I told you, like bitcoin, there are 21 million units. The problem: how do you know you can trust me? How do you know that I didn’t make 22 million units or 23 million units and kept some for myself or gave some to my friends. Or even if took none it for myself, what if I just honestly went about creating more currency, effectively creating a new central bank. How do you know, I’m not going to do that if I’m in control of it? There was no answer to that question, until there was a blockchain. With a blockchain, we can now authenticate every transaction. The whole purpose of bitcoin is centered around what happens when you have a fixed issuance currency; it’s supposed to function like Gresham’s law, which means, bad money drives out good. So, gold is better money than, let’s say, the dollar. A lot of people say that and I personally agree. […] In accordance with Gresham’s law, what people are expected to do – and which they do – is to hang onto their gold, and transact in or let go of their dollars. They’re not really supposed to use the gold for transactions, except occasionally. —- https://www.frmocorp.com/_content/letters/2022_Q3_FRMO_Transcript.pdf

This is not exactly true, but I think the video here explains the situation well enough:

https://www.federalreserve.gov/pubs/ifdp/1977/102/ifdp102.pdf

https://fee.org/resources/denationalization-of-money/

https://www.aier.org/article/cryptocurrencies-and-the-denationalization-of-money/

https://mises.org/library/denationalisation-money-argument-refined

https://cdn.mises.org/Denationalisation%20of%20Money%20The%20Argument%20Refined_5.pdf

Though Bitcoin does have a central team of devs, see https://bitcoin.org/en/development#code-review

An interesting debate on this can be found here, but since it’s hard to link to the exact location in the recording or transcript, I’ve quoted the relevant snippet here (you can word-search the actual transcript on the sight to follow the full discussion):

Mike Green:

The beautiful thing about Bitcoin is it fits every tulip in history. It is all things to all people. It is the mirror that reflects what you desire.

Nic Carter:

Yeah, I agree. I think that’s why it’s so difficult to discuss Bitcoin, is because it’s tinged with whatever your particular perspective is. I don’t see it as a corporate entity at all. I see it as an organic bottom up phenomenon. And if you’re Satoshi, I don’t see how else you would have designed it such that it could achieve this credibility and neutrality and issuance, aside from the way that he did it. And that’s the whole reason we’ve proof of work, because mining is costly, you have to surrender electricity in order to create new units of Bitcoin. The whole reason Satoshi designed it like that is so that there is no seigniorage, so that there’s no privileged class of people that have access to the monetary spigot, which is the case with other monetary systems.

Nic Carter:

So, because you have to burn $95 to get $100 worth of Bitcoin, it’s a free market competitive process and you have very slim margins, that means that the people that are creating the units don’t really have an advantage over the rest of the folks, so that’s how Satoshi did it. I mean, he could have emailed all the Bitcoins to the folks on the cryptography or cypherpunk mailing list when he announced it in 2008, but that wouldn’t have been fair, so he designed proof of work and included that into the system so that there would be this fairness in issuance. I think that’s pretty much the best possible way he could have done it. I can’t think of an alternative way.

Mike Green:

So if you’re saying there wasn’t a privileged class then why do we have several centimillionares or billionaires that have emerged out of the early days of Bitcoin before it’s even been proven?

Nic Carter:

Because they’re effectively speculators that made a very correct and very ballsy bet, basically. This is the case with any monetary transition, it’s always going to be disorderly. You’re never going to be able to airdrop the new monetary system pro rata to everybody on earth.

Mike Green:

But that’s, again, that’s ahistorical, right? Brazil introduced new currency, Germany introduced new currency, Japan introduced new currency. We’ve seen currencies introduced all over the world. They’ve never had the characteristic of a billion and a half drop to one individual and a few dollars drop to another individual.

Nic Carter:

You yourself said that Bitcoin is not a currency. And yeah, of course the state has discretion.

Mike Green:

But you just called it… Nic, you can’t go back and forth on this. You can’t call it a monetary system and then claim that it’s not a currency.

Nic Carter:

I mean, look, I think those are distinct, right? Like if you think currency is the purview of the state, fine, but yeah, certainly Bitcoin is a monetary commodity, so a system is absolutely what it is. But again, look, this is an organic phenomenon, it is new, because we have never seen new internet native monetary systems emerge from scratch before, because the internet didn’t really exist before, but cypherpunks had been trying to create digital cash for decades. Bitcoin was just the apotheosis of that. It was the conclusion of their efforts.

Nic Carter:

It was by no means the first one, there are a lot of failures before that, it was just the first successful one. But because we live in a world that’s rapidly becoming dematerialized, it shouldn’t be a surprise to anyone that we have an internet native currency. And under the circumstances, Satoshi distributed it in a way that was as fair as possible. If you want to get privileged access to Bitcoin, there’s no way you can do that. You have to mine it alongside anybody else and so you have to compete in the free market with mining.

Mike Green:

Yeah, unfortunately I actually disagree that. I think the evidence is very clear that it wasn’t distributed as fairly as possible. It was distributed to those with inside knowledge. Again, if I’d listened to my wife, perhaps I would be sitting on your side of the table, right?

Nic Carter:

She didn’t have inside knowledge, she had outside knowledge.

Mike Green:

That’s possible. Well, she is a woman and she is my wife and therefore she is going to be infinitely wiser in all situations.

Nic Carter:

Unless she’s part of the group that was Satoshi. But seriously, Satoshi announced Bitcoin in October 2008, gave everyone on that mailing list advanced notice. And then in January 2009 started mining Bitcoin. If Satoshi had wanted to sort of allocate themselves to share, they could have. They could have said, “Hey, I deserve 10% of this thing,” Which would have been a more corporate model. That would have probably been valid, but instead Satoshi just made it equal opportunity. It’s just that nobody cared about it and nobody thought it was going to succeed.

Mike Green:

It’s equal? Nic, come on. It’s equal opportunity? He distributed it to a mailing list. That’s no different than a friends and family insider route.

Nic Carter:

It was the most salient demographic, because it was an incredibly esoteric digital cash project.

Mike Green:

Yeah, I’m sure every Silicon Valley venture capitalist tells themself the same thing, that it’s an egalitarian spread amongst their friends.

Nic Carter:

It’s different.

Grant Williams:

No, but Mike, in fairness I’m with Nick on this, because I think this is something that if he distributed, Satoshi, to everyone in the world, most people wouldn’t care, they would have thrown it away or just ignored it. The people that actually cared and were engaged and were keen to build something from the ground up, we’re given some. But it was distributed among the people who cared about it, which I think is probably the best thing or it’s the fairest you could have been at the time, I think.

IMO, Green comes off as a prickly-for-no-reason Boomer and intentionally non-generous with any opposing arguments —more of a person debating to defend their own beliefs rather than someone trying to genuinely determine whether an investment is a good or bad idea; he literally calls Bitcoin “immoral” elsewhere in the podcast, which should give you a bit of heuristic info on how you should interpret his arguments and reactions, still an interesting listen overall, though.

********** UPDATE 20230522: An interesting article that I think articulates the issue with Green in particular can be found here: https://tftc.io/martys-bent/issue-1345/ **********

The Bitcoin development work / “IPO” was available equally to anyone in world for free (ie. anyone could mine all the block-reward BTC so lon g as they had heard about it), as opposed BTC having any “founder shares“ pre-allocated to the founding devs (eg. even the Ethereum founders gifted themselves what were essentially “founder’s shares” before its “IPO“)).

From the FY3Q2022 conference call (https://www.frmocorp.com/_content/letters/2022_Q3_FRMO_Transcript.pdf):

That being said, if you go to the blockchain explorer known as bitinfocharts.com, you’ll see, somewhere on that website, the Rich List. It’s a list of every public key—you can see it— who owns bitcoin, and you can view every transaction. You don’t know the names, but you can see every transaction, if you have the patience to look, that was ever done in the world of bitcoin. Based on my calculations—you can try to verify it yourself—87% of all the bitcoin outstanding is probably owned by fewer than 100,000 addresses. Moreover, I think that’s not even close to 100,000 people because we, at Horizon, for instance, have multiple addresses. I’d be surprised if it’s more than 23,000 to 25,000 people who own 87% of the bitcoin. It’s working exactly in accordance with Gresham’s law. The big holders rarely trade – that’s something you can observe on the website, too – and when they do, they’re almost always buying. They’re hoarding it because they know it’s going to have value in the future.

So, why in the world are they building these scalable networks for bitcoin?

You can see this website here: https://bitinfocharts.com/top-100-richest-bitcoin-addresses.html. If you click on any of the wallet addresses, you can see the wallet’s historical balance of BTC over time.

From the 2017 FRMO shareholder meeting (emphasis added):

Stahl: If it works, cryptocurrency would now be the money of society. By the law of no arbitrage, any of these currencies could have the value of a fiat currency, like the value of the Swiss franc or the Japanese yen, expressed in dollars. What is the value of Japanese M2 or M3? It’s in the trillions of dollars. Let’s say you start with a cryptocurrency worth, for the sake of the exercise, $5 billion, and set it against the value of the Japanese M2 or M3, whether it’s $2 trillion or $3 trillion expressed in U.S. dollars—I’m using these numbers just for illustrative purposes. Whatever the precise value of the Japanese money supply is today, they keep increasing it. Next year, it will be a higher number. So let’s just presume that a cryptocurrency with a market value today of $5 billion becomes $3 trillion. What’s the coefficient of expansion? It’s huge, right? You would have to multiply $5 billion by 600 to get to $3 trillion. So, you’d make 600 times your money.

According to Stahl this is best viewed by looking at the BTC price as a FX currency pair — which for US investors would mean having USd as the base currency like USD/BTC (how much BTC 1USD gets you), rather than BTC’s common form of being quoted as dollar asset like BTC/USD (how much USD 1 BTC can be converted to). From this POV, we can see BTC strengthening vs the dollar over time (as can be seen here).

Horizon Kinetics published a quick inventory of mainstream cryptocurrency adoption in early 2020, here: https://horizonkinetics.com/app/uploads/Cryptocurrency-Mainstream-Legitimacy_A-Brief-Survey-of-Institutional-Acceptance_April-2020.pdf

The link is timestamped to where he gets going into what he found so interesting about Bitcoin in the first place, but the whole interview is interesting. For the purposes of this article, a link to that interview timestamped to the part where Stahl rampd into what he found so interesting about Bitcoin in the first place is provided here:

https://player.captivate.fm/episode/3d0751dd-7577-450f-ad3a-1572264796e6?t=2019

I also find this to be a directionally interesting use case for Bitcoin: https://acceptingpayments.quora.com/The-0-00000001-Manifesto?ch=17&oid=4348163&share=5c24d2ad&srid=Pi3&target_type=post

This already exists in some form via the Basic Attention Token (BAT) developed by Brave Software in 2017 which seeks to build out a distributed micro/nano-payments ledger of crypto tokens minted on ‘proof of attention’ (to advertisements). It’s interesting and very much in the approximate ballpark of the idealized individual-to-advertiser disintermediation model. You can read more about it here and here.

Perhaps a token like Loopring would be a good bet in this case, see https://loopring.org/

I think that the behaviors of institutions are a good stand-in for general cultural consensus and from that POV we can — at least directionally — see Bitcoin’s percolating cultural acceptance via its slow march though the institutions here: https://pintu.co.id/en/academy/post/institutional-adoption-of-bitcoin-a-timeline

(There’s other more technical (and more debated) metrics, but this one is pretty good as a finger-in-the-wind, directional gauge, IMO).

Bitcoin — unlike actual gold — requires the internet to function; no internet, no Bitcoin. In this way, Bitcoin has a high beta risk to the maintenance and continuation of modern technological progress and general global stability. FYI: Just for a sense of scale on what I mean here — unlike what appears to be the case from much of the mainstream news — I don’t consider the ongoing RU/UA war to be a very significant risk to “general global stability.“

So in terms of Stahl’s reference to Law of No Arbitrage, it would seem like BTC’s market cap should really only be equivalent to the all of the savings in the world — not including the money actually in circulation through the economy. Which is why I align more with Matt Huang’s softer version of Stahl’s BTC investment thesis of BTC as a gold alternative (which I’ll cover in a later post).

Yet, at the same time, he’s also made statements in the not-too-recent past that appear to be in support of ease-of-MOE innovations in Bitcoin:

“So, if we as a society can enable people to easily transfer bitcoin, if a network were to develop sufficiently, I personally don’t see how anyone is going to prefer a government-issued fiat currency constantly being debased to a fixed issuance currency, a currency with a fixed reference point. The network exists right now, but it’s nowhere as easy to use as PayPal or Mastercard or Visa – but one day that’s going to happen. And when it does, the shift can happen in a very short period of time.” —- https://horizonkinetics.com/app/uploads/Quarterly-Commentary_Q2-2020.pdf

This is just a guess on the basis that BTC has fallen in price ~50% YTD and that GBTC made up around 15% of $FRMO’s TBV on a look-through basis as of their last quarterly report in late February (see “Investment B“) — so we’d really need to wait for the next financial release (I think in August) to assess the damage, but I think this should be approximately right so long as they did not buy the dip (which I’d be fine/OK with TBH).

If you can’t easily find it in the transcripts, here’s a snippet you can read as well as use to word-search the actual web page:

Yeah, I think it’s important because once you see the context you said, you really can’t unsee it. You start to really see the world through a new lens or a new, old lens maybe is the best way to describe it. So at the end of World War II, there was a monetary conference to basically set out what was going to be the new monetary system in the aftermath of the war. There were two options. There was the US option and there was the John Maynard Keynes option. And the US option was the dollar is the center of the universe. All other currencies are tied to dollar at various fixed rates or pseudo fixed rates and then very narrow bands. And then the dollar is pegged to gold at $35 per ounce. And Keynes’s proposal was something called the BANCOR, B-A-N-C-O-R.

And it was basically a basket of commodities designed to be a neutral reserve asset. And I think it’s a very important term, we’re going to come back to that later, it was a neutral reserve asset that was designed to settle trade between nations. And so if you were a creditor nation, you sold more than you bought, you ended up with surpluses, you would end up with BANCOR. You would end up with the ability to… You’d have the BANCOR. If you were a deficit nation, you would end up buying more than you sold. To settle that trade you would have to sell your currency and buy BANCOR.

So you’re selling your currency to buy BANCOR. Your currency’s going to weaken against the creditor nations. And so it would become a self-regulating trade system where the BANCOR is a neutral settlement asset that floats in all the currencies. Prevents major imbalances and at any rate, be a much more balanced, less crisis proof… Less crisis prone, excuse me, not crisis proof, but less crisis prone system.

TBH I find Snider’s style of writing and explaining things to be rather scattered, inscrutable, and meandering (though I may not be one to talk here), but I think what he has to say is still interesting (if I’m correctly understanding his scattered way to speaking).

********** UPDATE 20220922: Upon further review, I see that this is not exactly true, rather Stahl disputes the idea that gold could rise to a price that allows the US and other western countries to get out of their debt problems. Note this question was in the context of being asked during a Horizon Kinetics roundtable, where I assume this question was asked or written in, but IDK that I’ve ever seen mention of this idea by Pozsar himself. **********

********** UPDATE 20220930: Management addressed this in the most recent 2022 conference call as well as in the publication here. I’ve not yet made up my mind about whether I find this convincing. **********

********** UPDATE 20220930: Stahl answered this in the 2022 conference call, but not answered backwards/inversely re. my intention of the question, noting what was happening (vs the whether the current situation was such that it made sense for people to be acting in accordance with Gresham’s Law at all). Maybe it’s just my bias — that BTC is good gold, but not good money — that’s stopping me from understanding, but I don’t think so. **********

https://nakamotoinstitute.org/static/docs/denationalisation.pdf

https://www.perplexity.ai/?uuid=41596c0f-bec4-4611-b817-1d98ce9d2a42

Friedrich Hayek's denationalization of money is based on the idea that competition between different currencies will lead to the best currency being chosen by the market[1]. This is in contrast to Gresham's Law, which states that "bad money drives out good"[2][4]. Hayek argued that if people are allowed to choose their own currency, then "good money will drive out bad"[3][5]. This means that people will prefer to use a currency with a stable value and low inflation over one with a volatile value and high inflation. Therefore, Hayek's denationalization of money is based on the idea of allowing competition between different currencies, while Gresham's Law is based on the idea that bad money will drive out good.

2. Full article: Good money drives out bad - Taylor and Francis

3. Good Money Driving Out Bad: A Model of the Hayek Process ...

“That’s the divide between the academic and professional econometrics-based investment world and the practical world of applied investment analysis. […] Which is to say, informed estimation doesn’t need to be precise. A wrong answer can be precise to many decimal points. Informed estimation usually only needs to be approximately right – as to direction and magnitude – about the relevant few variables.” —- Steve Bregman, https://horizonkinetics.com/app/uploads/Q3-2022-Review-1.pdf

Using BTC network energy usage from here:

Assuming all 21MM BTC are already in circulation —not true and probably much less will ever be accessible due to key loses, etc, but just a simplification that I don’t think is too crazy

Taking a simple assumption that DoD energy use is 80% of total US energy consumption, getting the percentage value and US energy consumption value from:

“Since 2001, the DOD has consistently consumed between 77 and 80 percent of all US government energy consumption.” —- https://watson.brown.edu/costsofwar/files/cow/imce/papers/Pentagon%20Fuel%20Use%2C%20Climate%20Change%20and%20the%20Costs%20of%20War%20Revised%20November%202019%20Crawford.pdf (2019)

“The U.S. federal government consumed 915 trillion British thermal units (Btu) of energy during the 2017 fiscal year (FY), or 20% less than a decade before. The slight decline in FY 2017 marks the fifth consecutive decline in annual federal government consumption. Consumption by defense agencies accounted for more than 75% of total government energy consumption, according to data compiled by the Federal Energy Management Program (FEMP).” —- https://www.eia.gov/todayinenergy/detail.php?id=40192

“1 kilowatthour of electricity = 3,412 Btu” —- https://www.eia.gov/energyexplained/units-and-calculators/

Using the USD circulation value from here:

Thoughtful and earnest debate is one thing, but many seem bearish BTC to be a part of a group identity; they are just as invested as the BTC maxis, except they’re investment is emotional. Maybe they were once intrigued by Bitcoin and happened to arrive at a negative conclusion when they dug earnestly into it and are now as scornful, jilted lovers when they hear Bitcoin’s wretched name (which is nowadays hard to avoid), maybe they’re just cynical in their old age (and loud about it for some reason); in the case of the latter, I believe that off-handed cynicism is overused as a type of virtue-signal substitute for intelligence (often embarrassingly used by high-schoolers and old guys trying to feign worldliness). In any case, certainty is always cringe.